We’re Suffering From Health Care Stockholm Syndrome

For decades, the losers placed their trust, and dollars, in the hands of the winners, and went about their business. Health care costs were a once-per-year conversation and the goal was to get through it. Meanwhile, for the winners, health care was their business, and they spent every day trying to grow it. Now, we ask, has this unequal relationship reached its tipping point or are we all still all-in?

People like me have been saying for years that health care prices are unsustainable and insurers, hospitals, doctors, and Big Pharma should expect a backlash any day now. Wrong. Any day now has turned into ten years and insurers and hospitals are reporting record profits.

It’s So Hard To Say Goodbye To The Health Care Status Quo

Our relationship with the health care status quo has all the characteristics of an emotionally abusive relationship. The relationship started out well enough. About 100 years ago, Baylor University Medical Center in Texas offered a local teachers’ union a deal for hospital services. “For $6 per year, teachers who subscribed were entitled to a 21-day stay in the hospital, all costs included. But there was a deductible. The “insurance” took effect after a week and covered the full costs of hospitalization.” Soon, millions entered into insurance relationships, as the Blue Cross Plans expanded to other states. Continue Reading...

America's Third World Health Care Non-System Should Be Required Viewing

The first time I heard of RAM was in a 2008 interview with Stan Brock on the 60 Minutes television newsmagazine. Remote Area Medical and its thousands of medical and other professional volunteers, provides free medical, dental, and vision care to people who attend their free “pop-up” medical clinics. Stan Brock started the charity in 1985 to help people in third world countries get needed health care. But on that 2008, 60 minutes program, Stan was being interviewed about RAM clinics in Tennessee, USA.

According to a report in USA Today (2018), the United States is one of the wealthiest countries in the world in terms of gross national income (GNI) and gross domestic product (GDP)—ranked #11 and #2, respectively. America is not a third world country and it’s not remote, but somehow needs the free health care services offered by RAM. How RAM got to America is a story of unaffordable private and public (Medicare and Medicaid) health insurance. A significant number of Americans who receive RAM health care services, have or have access to health insurance but cannot afford the premiums and/or out-of-pocket costs the plans require. And many others do not know how to apply for low-cost or free health care.

Nothing says “failing private health care system” like the buckets of pulled teeth noticeable at any RAM event, or the thousands of people that line up the night before the clinics open in their area, to receive preventative health care. Which leads me to this: what if all Americans had to attend a RAM clinic once per year in exchange for tax-free health insurance premiums (employer group health insurance) and other government-subsidized health care benefits? It’s easy to love your private health insurance, as CNN.com likes to remind Medicare For All supporters. It’s hard to look at buckets of extracted teeth, made necessary because most private medical plans don’t provide preventative dental care. Continue Reading...

Health Care, Privacy, and Artificial Intelligence Collide (Into Possible Awesomeness)

In 2014, Google CEO, Sergey Brin, complained about “heavily regulated” health care that discouraged health care tech entrepreneurship. Last week Google emerged from secret talks with Ascension health system with a deal (Project Nightingale) to analyze and store health care and administrative data. Meanwhile, Amazon, who never shared Google’s timidity on health care, announced its third major health care venture in the last two years—the Amazon Care app. The rollout of the Amazon Care app for its Seattle-based employees comes after Amazon purchased online pharmacy PillPack in 2018 and teamed with Berkshire Hathaway and JPMorgan Chase to create the healthcare company, Haven. It seems like tech companies have found a remedy for health care’s regulatory headaches, or maybe it’s the chance for health care tech glory that they can’t walk away from.

There’s A Lot of Potential In Health Care Data Tech

It’s not surprising that Google changed its mind and inked a health care data deal. Google so wants to join the list of artificial intelligence (AI) pioneers, and having access to mounds of health care data is the first step to AI glory. Seriously, most health care systems around the world currently have AI projects to analyze health care data and monitor patients. And robotic surgery and robotic-assisted surgery has been a thing for well over a decade. Future AI health care projects may include machines that perform tasks currently done by health care professionals. When you think about it, the idea that if you compile enough data from multiple sources (doctors’ notes, physical exams, diagnostic images, etc.), you can teach a computer to diagnose and treat diseases is pretty cool.

Ascension also has a lot to gain if Google can manipulate the millions of patient data records into an AI system that can diagnose and treat diseases. Imagine the savings hospitals would realize if computers could replace some of the doctors and other health care specialists they would otherwise hire to perform these tasks. And it’s not just the potential savings of using artificial intelligence in health care, AI could reduce health care errors and allow hospitals to serve more patients.

Okay, I’m obviously fascinated by the possibilities of AI in health care. And if big tech can meet the privacy and security standards set by federal laws such as HIPAA, I say bring it on. We’ve already given up a lot of our privacy when it comes to health care. We’re willing to wear activity tracking devices, fill out online health risk assessments, and use telemedicine services all in the hope of improving our health or paying less for health care.

While Individual Privacy Concerns Decreases, Regulators Remain Alert

Ten years ago when I was working in private sector Human Resources benefits departments, health care data privacy was a big deal. Many workers balked at completing health risk assessments (HRA) because they thought their employers would use any “negative” health data from the assessment to fire them. They didn’t like the idea of their employer having such personal data. The Equal Employment Opportunity Commission weighed in on workplace wellness programs that charged higher health insurance plan premiums to workers that refused to complete a health risk assessment. Today, you rarely hear about health risk assessment privacy issues. But that’s not to say that privacy and security are not important in health care. The Health Insurance Portability and Accountability Act of 2003 (aka HIPAA) is a reminder to anyone who has or wants to access health care data of how seriously federal regulators take health care data privacy and security.

Between April 2003 and October 2019, the Department of Health and Human Services (HHS) received nearly 221,000 health privacy complaints. Continue Reading...

How Cruel Is Private Health Insurance? This Cruel.

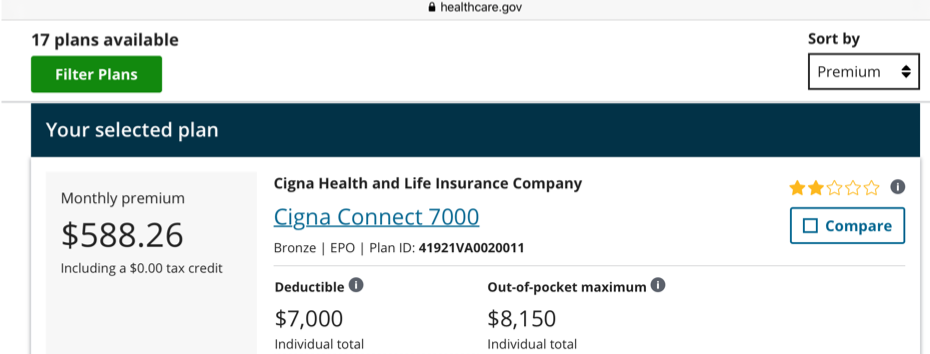

ACA Highest Cost Health Insurance Plan Option For An Individual - 2020/Virginia

The Healthcare.gov enrollment period started a week ago, on November 1. Like millions of people who must pay 100% of the health insurance premium insurers charge, I held my breath and prepared for the worst. Due to technological difficulties, I wasn’t able to log on to the site on the first day. No worries, there are benefits to delaying bad news. One is that you become irrationally optimistic.

Although it’s never happened before, I thought, maybe my individual private health insurance premiums would decrease. There are several reasons why they should.

- Last month I received a $99 refund, aka, medical loss ratio (MLR) rebate, from Cigna (based on Cigna’s 2018 MLR). The MLR rebate provision of the Affordable Care Act “requires health insurers to pay rebates to policyholders if the insurer fails to spend at least 80% to 85% of total premium revenue on medical claims and health care quality improvement activities (as opposed to administrative and marketing expenses and profits).”

- Cigna is financially strong. It’s 2019 third-quarter profits and revenues were up at $38.6 billion and $35.8 billion, respectively.

- The federal government’s Health and Human Services Department reports that health care premiums overall are decreasing in 2020.

- I’ve never needed medical care in my adult life. I’ve never been ill, injured, pregnant, or taken a prescription drug.

- I’m currently paying an extortionist, unsubsidized monthly premium for my Cigna EPO health plan (per my monthly email reminder).

“This email confirms that we have processed your Cigna health insurance premium payment of $564.33 on October 31, 2019.”

It’s The Government’s Fault. No, Not Really. Continue Reading...

The Financial Benefit Of High-Priced Health Care Is What?

Fast forward to 2019, and the average single and family monthly health insurance premiums (for a PPO plan) are $567 and $1,584, respectively.

Every year, purchasing life’s necessities gets exponentially harder as health care costs eat away at wage increases and savings. Even if you have enough money to cover your basic needs, paying $600 to $1,600 (or half of that if getting an employer and government tax subsidy), makes buying a car or a house, or starting a new business, impossible for millions of people. Other rich countries, and poor countries, too, realize this and have rejected overpriced health care. American employers, on the other hand, accept health insurance and health care increases as common practice.

Make Health Care Affordable For Employees, Not Just Employers

Employers are concerned, and even angry, about the never-ending annual health plan increases their insurers insists they need. They just aren't willing to take a really tough stand on the issue. And what would taking a tough stand on health insurance costs look like for employers? Employers should place price caps on insurance premiums and copays (we really need to eliminate deductible and coinsurance amounts).

When health insurers, hospitals, doctors, and drug makers realize that their biggest cash cow, employers, is no longer willing to pay what's billed, prices will come down. Medicare already says what it’s willing to pay and, to be fair; some employers are experimenting with variations of price caps e.g., (reference-based pricing). But small fry health insurance and health care price capping doesn't trickle down to the employee level, at least not enough to make health care and life’s other wants and needs affordable. Capping health insurance costs might also lead to greater health care price transparency. Do you want more money? Show us why you need it. We know you want it, but do you need it, and how much more? Continue Reading...

What’s Wrong With A ‘One-Size Fits-All’ Health Plan?

We’re Health Care Stupid…

Despite the efforts of employee benefits managers, consultants, brokers, communications and health care policy experts, Americans have limited health literacy—“the ability to obtain, process, and understand basic health information and services to make appropriate health decisions.” Surveys show that Americans know a lot less about health insurance than they think they do. A 2016 survey conducted by Policygenius, revealed that 96% of Americans don't understand the terms deductible, coinsurance, copay, and out-of-pocket maximum. A 2019 United Healthcare study, as reported by Motley Fool, showed that 90% did not know the insurance terms: premium, deductible, coinsurance, and out-of-pocket maximum.

It’s hard to make wise health care decisions if you don’t understand basic, cost-related health insurance terms that are part of most private health plans. We could eliminate premiums, deductibles, coinsurance, and copays under our current for-profit health care system. No one has to learn these terms. But instead of removing these terms from their health plans, employers and insurers have added more complexity. So-called health plan design innovations are the latest buzz in employer-sponsored health plans. Centers of excellence, reference-based pricing, high-performance networks, etc.: these cost-containment strategies replaced by one simple reform—one health care plan for everyone.

One Health Plan Is All We Need

Employers have it all wrong when it comes to health plan design. We don’t need a thousand different types of health plans, or health plan design innovations. A thousand different health plans require a thousand different documents that insurers must store in their systems. That equals more time spent doing system administration, and less time evaluating health care quality. If we had just one health plan: Continue Reading...

America Doesn't Want The Best Health Care For All

In 2016, I visited Russia, and in 2019 I visited South Africa and a few other African countries. St. Petersburg and Moscow, Russia were as cosmopolitan as any American big city, and the rural areas of Russia resembled some rural areas in America. Johannesburg and Cape Town, South Africa also resembled large American cities. There was nothing strange or exotic about Russia or South Africa. They are poor countries compared to the U.S., but unlike the U.S., they, at least in philosophy and on paper, look to provide health care to all of their citizens as a human right.

At Least “They"Support Universal Health Care

No vacation of mine to a foreign land would be complete without studying its health care system.

Russia and South Africa have major issues with health care access and quality. In the early 20th century, Russia provided free health care to all of its citizens, but later national reforms entitled “all Russians to free healthcare with Obligatory Medical Insurance (OMI). Employers contribute around 2-3% of employees wages into a social tax, of which a small proportion is put into a healthcare fund.” (So, not free.) In practice, however, many take out their own private medical insurance, known as Voluntary Health Insurance (VHI).”

The South African government, this month, “published a bill outlining a national health insurance program it intends to roll out over the next seven years. Private insurers will be able to continue operating until the system is fully implemented, after which they will only be able to offer coverage for services that complement those available from the state.

The current South African health care system includes a public and private system of hospitals and doctors. Funding comes from fees charged for services and government contributions.

The Russian health care system consistently ranks at the bottom among developed nations. It’s common to hear tales of drunken doctors, unsanitary conditions, and bureaucratic chaos. Russia’s private (market) health care system also struggles with quality issues.

South Africa’s public health care system suffers from a doctor brain drain (doctors train in South Africa, but leave to work in other countries), and sub par public health facilities.

If Only Americans Could Understand Health Care Continue Reading...

Employer-Sponsored Health Insurance Getting A Well-deserved Bashing

Stuck In Secrecy

Typically, employers have no idea what hospitals charge for their services. When hospitals agree to join a private health insurer’s network, the two parties negotiate their rates in secret. Neither the hospital nor the insurer shares this information with the groups paying the bills—employers and employees—until the bill is due. For their part, most employers never asked for this pricing information to begin with, and if they did, they still would not receive it. The majority of employers sign group health insurance policies or administrative services only contracts, agreeing that the insurance company does not have to reveal its "negotiated" network rates.

Health care price secrecy is unfair in so many ways. Imagine hospitals charging a different rate for the same service for each plan's network they join. That’s a lot of combinations of health care price secrecy. It can happen. One employer offering three "different" health plans could pay three different rates for the same service, provided by the same hospital. Also, these prices can vary glaringly across the country and in the same geographical area.

Workers Think Employers Are Negotiating Health Care Prices

It would shock most employees to learn that the “negotiating” of health insurance rates between their employer and the health insurance company, does not include a conversation about health care prices. Most employers pay whatever premiums or claims expenses the insurance company tells them to pay, with the promise that what they are paying is a discount. Employers take it on faith that the “discounts” are saving them money, but there’s evidence that’s not the case. Last year Propublica reported on a case where Aetna paid a hospital "more than three times the Medicare rate for (a hip) surgery and more than double the estimate of what other insurance companies would pay for such a procedure" because that was the price it negotiated to pay (in secret) with the hospital. The patient (a former Aetna employee and actuary) protested the price and shared his research with his former employer. Aetna replied, "The payment was appropriate based on the details of the insurance plan." Continue Reading...

Employer Sponsored Health Insurance Gets A Well-Timed Critique

Imagine yourself in a bar where a pickpocket takes money out of your wallet and with it buys you a glass of chardonnay. Although you would have preferred a pinot noir, you decide not to look that gift horse in the mouth and thank the stranger profusely for the kindness, assuming he paid for it. You might feel differently, of course, if you knew that you actually had paid for it yourself.

A New Day Brings New Scrutiny To Workplace Health Plans

Last month, an article by Drew Altman, titled, For low-income people, employer health coverage is worse than ACA, explored workplace health insurance affordability issues for low wage workers and workers with chronic illnesses. Altman writes:

We tend to think of everyone with employer coverage as one big group, but it’s really lower wage workers — and, while it’s a different subject, also people with major illnesses — who take it on the chin in the current private health insurance system. They are also the group with employer coverage who would benefit the most from a Medicare-for-All style plan.

The bottom line: Employer-based coverage is by far the largest source of health insurance, and it now provides the least financial protection for lower income workers who need it most.

Altman gets to the heart of the matter when he writes, "We debate affordability in the ACA marketplaces a lot, but we don’t talk about this far larger problem much, if at all."

A week after Altman's article, a report from The Foundation for Research on Equal Opportunity (FREOPP)—a public policy think tank co-founded by Obamacare critic, Avik Roy, designated employer sponsored health insurance as the worst form of private health insurance in the country in terms of underlying cost, sustainability, freedom of choice, and consumer-driven incentives. Worse than individually purchased health insurance, federal employees health benefits, and Medicare Advantage—the country’s other private health insurance programs.

No More Hiding

Employers Are Ready To Innovate Their Health Plans. Insurers Don’t Care.

Large Employers Are Tinkering With Their Health Plans And Calling It Innovation

If you read about health care even occasionally, you know about the new company, Haven. A venture created by the heads of Amazon, Berkshire Hathaway, and JPMorgan Chase. Large companies that got together to create a health insurance company with the goal of lowering health insurance and health care costs for their employees. The health insurance status quo said, have at it. Private health insurers know better than most what’s required to make health care more affordable—medical care price controls and health care trade-offs. Insurers have perfected the art of managing health care trade-offs—most benefit plan documents contain pages of excluded health care benefits. And since employers aren’t talking about price controls, with the exception of reference based pricing, which is technically a form of price controls but with numbers that are easy to manipulate, insurers aren’t that pressed about this new wave of employer health care “innovation.”

Still, we don’t know what “innovations” to expect from Haven, but based on what I’ve read so far, it involves technology. And Haven’s not the first group of large, wealthy employers exploring how technology can help control health care costs. According to a very informative article in Benefits News, before Haven, there was The Employer Health Innovation Roundtable (EHIR), “a grassroots group made up of nearly 60 of the country’s biggest employers that represent nearly 8 million employees.” This group includes mega companies such as Apple, Target, and Google. Basically, representatives from EHIR watch presentations from health care tech start-ups and decide if they want to pilot the “benefit” at one of their companies and report back its findings to the large group via case study or some other format. Continue Reading...

We Should Not Reward Large Employers For Making Health Insurance More Expensive And Less Accessible For All

It’s A Bro Thing, A Control Thing, And A Money Thing

It was just over one year ago that Amazon, Berkshire Hathaway, and JPMorgan Chase announced their joint health care venture. The three business giants said they were combining forces to “provide low-cost, high quality service from a (health care) company ‘free from profit-making incentives and constraints.” But soon after the announcement one of the Big 3, JPMorgan Chase CEO, Jamie Dimon, promised not to compete with private health insurers and would instead restrict the new venture’s efforts to helping the employees of the three companies. We know why Jamie tried to walk back his threat to upend private health insurance—some of his company’s clients are in the health care industry—but why do other major companies support the industry, and do not publicly support Medicare For All?

I can think of a few reasons.

Despite surveys showing that health care costs are a major concern of all private companies, large companies seem to prefer private health insurance to a government-run or universal system. No major corporation has cut all ties with the health insurance status quo. Instead, corporations work with major health insurers to support each other's profits and shareholder returns at the expense of the country. Also, many leaders of “American industry” believe that they know more about health insurance and health care than health care policy analysts, government officials, and economists. They think the private sector is just generally better at running any business even if it has public policy implications. Continue Reading...

Time’s Up On Secret Price Negotiations Between Private Health Insurers, Hospitals and Doctors

The Public Has A Right To Know What It's Getting For It's Health Care Dollars

The Trump Administration, according to a recent article in the New York Times, said, "it wanted to require public disclosure of the rates doctors and hospitals negotiate with health insurance companies." The operative words here are "wanted to require," this is not a formal proposal, according to reporting in the Wall Street Journal. But just wanting to broach the subject around the transparency of contracted rates between health insurance companies and hospitals and doctors is groundbreaking. After more than half a century of purchasing health insurance, employers never asked, at least to the public's knowledge, for this information, even though they and their employees are the true payers of health care.

As someone who worked in HR benefits departments of private companies and participated in annual health insurance negotiations, I have to admit I never requested information on insurer negotiated discounts with network providers. I wanted to know, but I took for granted that the discounts were significant and that it was in the best interests of the insurer to negotiate a “good deal” with the hospitals and doctors in the plan’s network. I’ll never know if the health insurance companies negotiated in good faith on behalf of my employers, but I have reason to be skeptical.

Private health insurance companies haven't behaved like insurance companies for decades. Self-funding by employers means no risk for the insurer, unless claim costs exceed the insured stop loss limit. And high premiums based on secret negotiated discounts for fully insured health plans ensure profits, not losses for the insurance company. The one health insurance product that may result in a loss for insurers is an individually purchased private health plan, which before Obamacare, was highly restrictive due to preexisting condition exclusions, excluded benefits, and premium costs. Post-Obamacare, sky-high premiums and deductibles for individually purchased health plans greatly reduce insurance company risk of loss.

It’s Not An Equal Relationship

Recent reports about some health insurance brokers and some private health insurance companies reveal that these brokers, often hired by employers, in effect work on behalf of the insurance company. Broker compensation and bonuses come from and are contingent upon selling the health plan to the employer and retaining that employer’s business year after year. Other reports show collusion with hospitals and doctors to set discounts on inflated medical care rates. Still, even large employers haven’t requested the discount information the Trump Administration is contemplating. Instead, they are working with consultants to help them create their own private networks (Amazon, Berkshire Hathaway, and JPMorgan) where they negotiate rates for medical care services directly with hospitals, doctors, and drug manufacturers. Continue Reading...

We Must Fight Against The Health Care Status Quo's Propaganda War on Medicare For All

Health Care Industry Anti-Medicare For All Ads Are Pathetic

Social and other media outlets are currently awash in anti-Medicare For All ads, funded by health care organizations and other businesses.

The Partnership for America's Health Care Future (P4AHCF), recently sent out a tweet warning of a future of high prices, low quality, and fewer health plan choices under Medicare For All. (Someone should tell them that the future is now.)

→ https://t.co/Z5Z50kYzm0 pic.twitter.com/JEHK0bKqJU— Partnership for America's Health Care Future (@P4AHCF) February 25, 2019Between the higher price tag, the lower quality care, and the loss of choice and employer-provided coverage, a “one-size-fits-all health care solution” is hardly a solution at all. Learn more

And there's more. The P4HCF's web site has this to say about our current health care system.

"While our current system is not perfect - we know there are many parts of it that are working well for patients across the country. And thanks to ongoing progress, we can continue to build upon and protect the parts of this system that work well - while improving up the parts that do not."

Aside from the strange "improving up the parts" wording, The Partnership's using the tried and tested tactic of holding up the employer-sponsored health insurance market as a model of success. It's not, and it deserves an honest response.

Employer provided health insurance is not a success, it is not a part of the system that works well, and it is not relatively inexpensive as some may think. Employment-based plans receive favorable tax treatment that limit what employees pay, as well as subsidies from the employer. That $1,200 annual premium that the employee pays may receive a subsidy of over $4,800 from these two sources, leaving the employee with the false belief that their health plan is inexpensive. Health care spending in America consumes over 18% of the country's gross domestic product (GDP). It is not inexpensive. Continue Reading...

The Battle For Equality In Health Is A Battle For Equality In Life

Just look at how they've responded so far.

Appease: Trump, unwilling to admit defeat to Nancy Pelosi, agrees to temporarily not get his way.

Ignore: Michael Dell, CEO of Dell Technologies and billionaire attendee at Davos, says voluntary philanthropy is a better solution to inequality than taxing the uber rich. (Like that's worked so far.) He also falsely claimed that increasing rich peoples’ taxes hurts economic growth. Bottom line: Mr. Dell thinks that he knows better than the government how to “fix” inequality.

Appease (with a catch): Microsoft, responds to years’ of criticism for exacerbating the affordable housing crisis in the city of Seattle, by creating a multi-hundred-million-dollar housing loan program, along with a much smaller grant to address homelessness. This is a loans-to-pay-for-future-loans program in lieu of higher taxes; with a much smaller grant program thrown in to make it appear more generous. (Where does this I know how to address housing policy issues better than government attitude come from?)

Appease (latch onto): Health insurers and hospitals, in an attempt to forestall Medicare For All, are rolling out small-scale programs to address social determinants of health—‘the circumstances in which people are born, grow, live, work, and age’ that affects their health status and leads to health inequality. (Marmot, Sir Michael, The Health Gap (The Challenge Of An Unequal World): Bloomsbury Press, 2015). By making a small financial commitment now against health care inequality, which was never a major concern of theirs, health insurers and hospitals, hope the public will ignore their ever-increasing, opaque prices and poor health outcomes, on the part of hospitals and doctors. Continue Reading...

2019—A Health Care Revolution Is Coming

Meanwhile, people who have health insurance don’t want to use it because even with insurance, they may have to pay high medical bills when they receive care. Other people, especially in the individual health insurance market, are going without health insurance. After years of paying thousands of dollars each year in insurance premiums and deductibles, they have nothing else to give. Which makes me wonder: with all the frustration over ever-increasing health insurance and health care prices, will 2019 be the year the health care status quo loses its political and cultural support?

It’s On! (The Health Care Value Debate)

Maybe it's me trying to deal with the anger I feel about the 25% increase in health insurance premiums Cigna gifted me this year, but I’m starting to get a sense that 2019 won’t be business as usual for our greedy health insurance and health care industries. Or maybe it's a number of other signs I’m seeing in the health care reform policy debate:

- The new Democrat-led Congress elected to protect health care access, address health-insurance and health care costs, and explore universal health care options like Medicare-For-All or Buy-In, and Medicaid-For-All or Buy-

- The growing demand for real health care price data and all-payer claims databases by individuals and state governments, respectively

- The consistent reporting of and angry responses to outrageous medical care costs like the $629 Band-Aid, $4,000 surgical screw, and $52,000 per month prescription drug

- The study of health care value both nationally and internationally—what are we getting for the trillions we are spending, and what’s the real cost of innovation

Resistance Is Futile, But It Will Be Fierce Continue Reading...

How Workplace Wellness Can Regain Its Credibility

Employers that want to offer credible, research-driven wellness benefits should follow the lead of public payers and incorporate socioeconomic screenings and benefits into their wellness programs.

Workplace Wellness Programs—Entrenched and Evolving

According to the Kaiser Family Foundation, 49% (157,381,500) of Americans were covered by employer-sponsored health plans in 2016. In addition to their health insurance coverage, many of these individuals have access to an employer-sponsored wellness program. Despite the growing cynicism about the efficacy of workplace wellness programs, they don’t seem to be going away.

Wellness programs have expanded and evolved from weight loss clubs, health screenings, fitness challenges, and annual flu shots to onsite health clinics, fitness trackers, and financial counseling. So-called innovative wellness programs at top companies like Google, Motley Fool, and Zappos, provide nap rooms, Ping-Pong tables, massages, weekly recess, and other unique perks. But what started as common-sense promotion of healthy behaviors has turned into an unconnected, mix of wellness benefits without thought or impact. However, there may be a way for workplace wellness programs to redeem their legitimacy.

Getting Serious About Workplace Wellness Programs

If workplace wellness wants to return to its serious origins, it should look to the important work taking place in the public health care sector—screening for and addressing social determinants of health (SDOH). The Healthypeople.gov website defines social determinants of health as, “conditions in the environments in which people are born, live, work, learn, play, worship, and age that affect a wide range of health outcomes.” Specifically, SDOH includes factors such as income, education, food, environment, transportation, housing, and race and ethnicity.

Employers may think that confronting socioeconomic issues is an invasion of their employees' privacy, and that this work is best left to public policy experts. This is a legitimate concern; however, as the second largest payer of health care in the country, employers should not wait until government or some other group does the work for them. At a minimum, employers should become familiar with SDOH research, and incorporate socioeconomic screenings and benefits in their health plans and wellness programs.

Private health insurers can serve as a resource for employers that want to address socioeconomic issues through their benefits plans. Insurers (BCBS, UnitedHealthcare, Cigna, and Aetna) have experience creating tools and designing SDOH benefits for their Medicare and Medicaid enrollees. Some SDOH benefits employers should consider including in their health plan or wellness program include: Continue Reading...

Health Care's Biggest Problems Are Not About Technology

Improving Services And Saving Lives

Oscar’s social media branding approach to health care and real-time data decision tools are a welcome contrast to the everything-but-the-kitchen-sink websites of other health insurers. A system that uses real-time prior authorization for surgeries is a huge improvement over faxing forms and waiting days or weeks for a response from the insurer before you can schedule an appointment. An insurance company that pays claims in real-time, while you’re still at the doctor’s office, is much better than waiting for a bill from the doctor and then waiting for the insurer to pay its portion before you know what you owe.

Innovative technology is good for the health care industry and the trash-talking bros at Oscar (these guys can't get through an interview without a negative comment about their competitors’ antiquated legacy systems) are producing tech that improves the health care experience and has the potential to save lives.

We know that the technology doctors and hospitals use to diagnose and treat patients can save lives, but so can having immediate access to real-time data. A recently reported story on Forbes Online about an Australian cancer patient, Mettaloka Halwala, illustrates how faxing forms can result in medical errors. In Mettaloka’s case, it was a death sentence. Less serious, but still frustrating, administrative errors occur in health care every day. Since 2014, Blue Shield in Los Angeles’s enrollment system, the one used for individual health plan purchasers, has been on the fritz. The enrollment system unexpectedly terminates policies of individuals whose premiums were paid. Customers spend hours on the phone trying to get their insurance coverage reinstated, all while skipping medical appointments and delaying prescription drug refills for days, weeks, and months. Blue Shield in LA’s continual system problems for the most basic of services is one of the worst examples of a major health care industry customer service failure due to inadequate technology.

Big Data, Innovative Tech, And The Human Condition

The rollout of the Affordable Care Act (aka Obamacare) had its technology challenges. But the Act achieved its primary purpose of providing affordable health insurance coverage to the millions of people without coverage. A glitch-free enrollment system, impervious to attack by political rivals, would have been a good start for Obamacare supporters and enrollees, but, what’s more important—affordable coverage or a streamlined health plan enrollment system? The guys at Oscar might think that they are providing both, but are they? Using data analytics, predictive modeling, and artificial intelligence may eventually lead to administrative savings in health care, but other factors can replace those costs. Continue Reading...

Employers Are All In On Maintaining The Health Insurance Status Quo

You would think that large employers would say to heck with the health insurance and health care status quo. You would think that they have had enough of the annual negotiation performances played by brokers, consultants, and health insurance representatives. You would think this, but you would be wrong. Large employers are generally opponents of a single-payer (e.g., Medicare For All) system that would replace their private group insurance plans. They may not enjoy participating in the ritual pretense of controlling health insurance costs, but they find it preferable to the alternative—losing control of a powerful financial tool.

There are several reasons why big companies and the health care industry do not support Medicare for All or single-payer health insurance.

Large organizations that are not part of the health care industry oppose single-payer because they would no longer be able to use health insurance as a recruitment/retainment tool, or as way of manipulating the total compensation their employees receive. These organizations may also benefit financially from health care industry stocks. And you've got to figure that large corporations don’t want to upset each other because the shoe could easily be on the other foot, so it is best to have each other’s backs.

Health care organizations have even more at stake in the single payer debate. According to a Kaiser Family Foundation report, health care employment accounted for about 9% of all employment in the U.S., in 2017. The industry, with the exception of some groups like Physicians for a National Health Plan (PNHP) and a few others, vehemently opposes single-payer health insurance. The Healthcare Leadership Council, a health care industry lobbying group, lists insurers, hospitals, drug makers, medical device manufacturers, pharmacies, health product distributors, and information technology companies as part of the health care industry. Add to that the thousands of companies and freelancers that support these organizations... The bottom line is that the health care industry employs millions of people, and makes tons of money for Wall Street—a gig they would like to keep.

Small Employers Will Save Us

Health care reform isn’t over. Everyone agrees that health care costs is THE problem we must resolve, and that the solutions proposed by insurers and adopted by private sector organizations large organizations are band aids. So far the reforms taken to make health care more affordable and available involve transferring costs from one group to another. Large organizations can play this shell game better and longer than smaller companies because insurers realize from time to time they have to let the big guys win (or think that they've won). Small employers on the other hand do not have this kind of clout, and usually follow the lead of larger organizations when it comes to plan design, financing, and other health insurance reforms. Continue Reading...

Are Employers Growing Wary of Their Health Insurance Partners?

So far the public response from big health insurance company CEOs has been diplomatic. Cigna CEO, David Cordani, stated in multiple interviews with the financial press that he sees the venture as "an opportunity." Aetna's CEO, Mark Bertolini, also to the financial press, said, “There is an unmet consumer need in health care." And UnitedHealthcare CEO, David Wichmann, said, "We invite innovation in health care." But Wichmann also said, "Our goal is to help people and make the health system work better for everyone. If Amazon can contribute to that, they should bring it." This refreshingly honest statement from Wichmann and his singling out of Amazon, implies that at least one big insurer considers the new company to be a competitor. But it is the sentiment expressed by outgoing CareFirst BCBS CEO, Chet Burrell, when he said, "What exactly are they going to do differently?" that is mostly likely what the big insurers are all thinking.

With Friends Like These

How long did health insurers think they could hand-deliver products that cut costs by shifting it to employers and their employees? Large employers were early adopters of skin-in-the game cost-cutting strategies like PPO and HDHP plans and know the limits of these schemes. Now, these employers want to see lower health care prices, which means health care insurers have to step up their game. To lower health care prices for their employer groups, insurance companies have to get greater price discounts from hospitals, doctors and pharmacy benefit managers, not just focus on employee behavior. Continue Reading...

Knowledge Isn't Power When Managing Health Care Costs

Both the KHN/NPR and Vox projects started in 2018, but stories about inexplicably high medical bills are not new. Major news organizations have been shocking readers with reports of shameless health care price gouging for years. Journalist, Steven Brill's 2013 article, "America's Bitter Pill…" in Time Magazine, grabbed the nation's attention like no other health care price article has before or since. In fact, Brill's blockbuster article likely inspired NPR and Vox's current medical bill review projects, as well as several bestselling books on the subject.

Meanwhile, a similar information campaign about income/wealth inequality is also cause for outrage. But if the response to news about income/wealth inequality is any indication, what can we expect the stories about health care price gouging to accomplish? Remember Occupy Wall Street and Fight For $15—how participants in these movements were mocked as naïve losers out to take from the makers? And how Republican lawmakers enacted tax cuts for corporations and wealthy individuals to punctuate the defeat of these groups? It's not hard to believe that this is the fate of the health care price outrage campaign. For every successful teachers' strike there is an annual health insurance premium increase to gobble up any negotiated benefits increase. Continue Reading...

Stop Praising Health Insurers For Raising Rates "Just A Little"

Steady,

Still, you may be thinking that a slowdown in health insurance premium growth is good news or you may be thinking, what's the harm in saying things are better than usual. Where to start?

First, news of lower than usual health insurance premium increases applies mostly to large employers. Smaller employers will continue to see rate increases in or approaching double digits. Second, these "slight" rate increases are made possible by already overinflated health insurance rates. Individual premiums for some small group health plans can be as high as $700 to $1,000 per month, based on benefits covered and cost-sharing structures (e.g., deductibles, coinsurance and copays). These rates are higher than the exchange rates.

But the number one reason we should not celebrate lower than usual group health insurance premiums is that it gives a false impression that we are controlling health insurance and health care costs. That employer groups have finally figured out how to win at the health care negotiating table. That health insurance companies are more accurately predicting risks and passing on the savings to their employer groups. That workplace health insurance is a bargain and operates like a fine-tuned machine, not in need of reform. That health insurance prices are not something we need to address, at least not right now. Nothing could be further from the truth.

Steady Rates or A Red Flag

There is no reason to believe that health insurance costs are under control or are a minor issue in the whole health care reform debate. The cost of health insurance (and health care) is the debate. Health insurance prices are too high and individuals can't determine the value of their policies.

Also, if health insurance was becoming such a bargain, why don't health insurers share price and discount information with the public or employer groups? If insurers are paying providers four, five or six times the Medicare rate for medical services and receive a 50% discount on less, that's no bargain. And if insurers charge a little less to access these inflated, low discount rates, why give them a pat on the back? Continue Reading...

Real Health Care Reform Requires A Price Reduction Conversation

After weeks of silence, followed by news of Obamacare sabotage, health care reform policy returns to center stage. Last week,

The Sanders plan is long on moralizing (yes, health care should be a right) and short on concrete ideas to address health care costs. The plan includes all of the usual policy proposals to lower health care costs: administrative simplicity, enhanced negotiating power with prescription drug makers, federal subsidies for health care worker training, incentives for doctors to provide better care, and making rich people and employers pay more of the costs for national health care. The only thing new about the Sanders Medicare for all plan is that now it is official.

The Graham-Cassidy et al plan put out by Republican Senators Bill Cassidy (a doctor), and Lindsey Graham is a lot like other Republican health care reform proposals of late in that it looks to reduce federal funding of health care by replacing current subsidies with smaller block grants. The bill would also reduce the amount of money the federal government gives to states to fund their Medicaid programs. But mostly the bill, if passed, will unabashedly, take health care away from millions who currently have it with no pretense of offering them anything in return. There's more awfulness to read in Cassidy-Graham, but the overarching message is that Americans do not have a right to federally funded health care.

So here we are, again, with two opposing policies on American health care reform. Meanwhile, big pharmaceutical companies continue to introduce drugs approaching or surpassing the half a million-dollar cost mark. Employers persist in maintaining health plans whose costs they cannot manage. Workers' keep on watching health care premiums eat up their small wage increases. Politicians continue to move money around from one powerful health care interest group to another. And Americans continue to fall for the you-can't-put-a-value-on-your-health and the importance of American innovation cons to justify uniquely high-priced American health care.

No Shame In the Health Care Price Game

No one disputes that America has the highest medical care prices in the world. But in typical American fashion, some of us like being at the top of even this list. Defenders of high-cost American health care claim the costs are high because we as a country can afford it, and that that's the price tag for medical and drug innovation. But neither of these claims is necessarily true or right. Tens of millions of Americans cannot afford to pay for health care, and the high price of medical innovation shouldn't go unchallenged.

Last week there was a report about a new cancer drug with a $475,000 price tag. And it seems like just last year we in awe about a new Hepatitis C drugs that cost about $80,000 per patient. Also, just two weeks ago, Texas Medical Center was bragging about its $50 million worth of floodgates protecting it from Hurricane Harvey. Yes, America obviously has a lot of money to invest in medical care, but is it investing it wisely, is the greatest number of people helped by these investments and who gets to make these decisions. Continue Reading...

Affordable Health Care Is No Where In Sight

Don't be fooled. After finally

Unfortunately, and despite the latest CSR payment, Trump and Price's sinister plot to undermine Obamacare is having the intended effect. Because health insurers cannot be certain that this Administration will not stall or stop future subsidy payments, they will increase rates by a higher percentage than they otherwise would have. And when health insurers feel uncertain and are afraid they won't meet their financial objectives, they take it out on everyone. That means health insurance premiums may be higher for everyone next year, even employer-sponsored group health plans.

But that is not all on Trump and Price. Their childish, mean-spirited antics only highlight a fundamental problem with a for-profit, private sector led health insurance industry. You see, American health insurers have always insisted that their profits be assured. Taking a loss in one line of business (selling to individuals) and making it up in another line (employer-sponsored and other group insurance), but still making an overall profit, is viewed as a loss for them. They want all of their lines of business to be profitable all of the time.

Even if Trump and Price admit that the Republican health care reform efforts have failed, that they will now honestly administer the Obamacare law as intended, and promise to make all future CSR payments on time, insurers will still raise rates higher than are needed until they feel comfortable that their profits will continue. How long will they wait until they are comfortable that their profits are not in imminent danger? They will wait as long as they want to, which is forever, and there is nothing we can do about it.

Health Insurers Will Always Inflate Premiums

It is so disingenuous for Obamacare critics to imply that the health insurance market was ok or even better before Obamacare. How they ignore or explain away that purchasing individual health insurance pre-Obamacare was hit or miss or that finding comprehensive and affordable coverage was impossible is beyond my comprehension.

Purchasing individual health insurance pre-Obamacare was a long and difficult experience. First, you had to find a reputable insurer that sold individual plans, and then you had to work with an insurance broker to apply and purchase the policy because you couldn't work directly with the insurer. And that describes the not too bad parts of that old way of purchasing insurance. The fact that tens of millions could not purchase individual health insurance, some because they didn't want to, but many because they were denied or couldn't afford it, tells you everything you need to know about why Obamacare or something like it was bound to happen. Continue Reading...

Tax-Free Health Insurance For All Is An Easy Obamacare Fix

As Donald Trump puts his limited energy into showing the world that this presidency thing is way beyond his limited abilities, the insufficient patches to the American health care system lumber into another year. More of the same high-cost but accessible health care is a better deal than what Republicans were offering with their

Republicans lawmakers are not the only ones that waited seven (7) years to suggest changes to the Affordable Care Act (aka Obamacare), Democrats did too. And, to add insult to injury, they callously repeated that the number of non-subsidy receivers was so low and, if you thought about it, these people could technically afford high-cost insurance. They also promised to eventually come up with a solution to this minor Obamacare problem. Well, after 7.5 years Democrats have yet to propose one suggestion to the non-subsidy problem for the millions stuck with paying 100% of high-cost health insurance. However, strangely, there is a law that was passed by both Republicans and Democrats that could help these individuals, including me, but by design, does not.

Say QSEHRA, QSEHRA

In December 2016, a nearly unanimous Congress passed the 21st Century Cures Act. This Act includes a provision that allows small employers to offer a flexible benefits plan, called a qualified small employer health reimbursement arrangement (QSEHRA), to help their employees pay health insurance premiums and health care expenses with tax-free dollars. One way a QSEHRA works is an employee purchases an individual policy, pays the premium out of their pocket and submits proof of coverage to the employer who has set up the QSEHRA plan. The employer reimburses the employee for the premium, with tax-free dollars, up to a mandated amount. Or, if the employee has coverage through a spouse’s plan, the employee can receive tax-free reimbursement to cover medical expenses. The QSEHRA regulation changed the way health reimbursement accounts were treated under Obamacare as it was designed to help small employers provide premium and health care cost assistance to their workers when providing health insurance was not financially or administratively possible. Continue Reading...

Talking About Highly Paid Doctors Does Not Devalue Their Work

Becoming a medical doctor in the U.S. is very hard. It takes years of study. We know this because doctors are great at reminding the rest of us of the costs they incur and sacrifices they make in pursuit of their medical degrees. Also, let’s not forget, because they won’t let us, that doctors help the sick and save lives. Don’t get me wrong; I’m not trying to undervalue the efforts and commitment of doctors. However, I’m also not willing to exclude doctors from criticism for the role they play in our overpriced American health care system.

If Medicine Is Noble, Not Every Doctor Is

Medicine and money go hand in hand, and so does greed and self-importance. Some doctors enter the medical profession for noble reasons—they want to alleviate illness and save lives; for others, it is a pathway to wealth and prestige. And no one exemplifies the greedy, egoism of the medical profession like Health & Human Services (HHS) Secretary Tom Price. Now a politician, Price was once an orthopedic surgeon and director of an orthopedic surgery clinic in a wealthy area of Atlanta, GA. Orthopedic surgeons are the highest paid of all medical specialists, with an average salary of nearly half a million dollars a year.

Tom Price was never shy about wanting to become a wealthy doctor. It was his goal. And even after moving into politics as an elected Congressman and now head of HHS, he continues to invest in the health care industry and lies about his corrupt investments in the medical field. Another thing Price never lies he doesn’t lie about is his views that doctors should be left alone to make as much money as they can make. At HHS, Price is looking out for doctors’ pocketbooks. In Price’s world, Medicare payments to doctors rise, quality standards and medical malpractice awards go down, and electronic health records disappear (because who wants to share data with other physicians and invite competition). And that’s not even the worst of Price’s financial activism on behalf of his fellow doctors that don’t want to change but want more money. Price wants to collaborate with doctors in letting them decide how much Medicare (taxpayers) pay for their services.

It Matters Who Becomes A Doctor Continue Reading...

Medicaid For All Will Make Health Care Just Another Commodity. So What!

I finally agree with what health care policy writers have been saying for months—An American

And to make it clear on where they stand on this impending new health care world, they are reviving their objections to the “provider” label. Although decades old, doctors hate the provider label now more than ever. They find the use of the term condescending because it links them with other medical care professionals like nurses and physician assistants—people not at their level of expertise. But the primary reason many doctors dislike being called “providers” is that they see it as a “commoditization of the doctor-patient relationship” and now you’re messing with their money.

Commoditization refers to the process by which goods become so similar that their only distinguishing characteristic becomes price. The development of tablets and smartphones are an example of commoditization. They all have the same or similar features like touch screen and syncing with other devices, etc. And even though I prefer Apple products and give the company credit for pioneering much of the technology now available on other devices, I know that I could accomplish pretty much the same tasks with a non-Apple tablet, phone or computer and at a much lower cost.

Apple is not afraid of commoditization; it expects and thrives in this type of environment. It sees the competition as good for customers because it pushes the company to innovate more. Doctors, on the other hand, hate the idea of commoditized health care. They don’t want to compete on service or price. In fact, the real reason doctors and hospitals don’t want electronic medical records or to publish their prices has nothing to do with costs but because they are afraid a competitor will “steal” their patients if they had access to this data. And, of course, doctors think that their product (health care services) is unique

To date, we have protected doctors and hospitals from real competition and allowed them to charge whatever they want for their services. A Medicaid or Medicare For All single payer health care system that includes electronic medical records and price transparency will force doctors and hospitals to compete on price. This type of system is good for the public because it’s one of the few ways, other than forced price reductions, to make health care affordable. Doctors and hospitals won’t like this more transparent health care system, but who cares; it’s coming, and they know it. Continue Reading...

America's Health Care Identity Crisis

About every July 4th or after a presidential election writers try to explain the American Identity. Some of them, especially of late, conclude that the American Identity is in crises. America does not know who she is. Others say America knows who she is—she is freedom of speech, religion, and opportunity. America is individualism. If there is an American Identity crisis, it is because we have replaced these freedoms with government interference.

There's no denying American democracy is under attack, but ironically our present debilitating state has crystallized our identity. As the

America is a place where:

- Slumlords rent substandard, barely habitable housing to the poor because people will pay to live there

- Payday lenders, check-cashing centers and prepaid debit card providers keep the working poor in a cycle of debt offering services traditional banks will not

- Children, under strict rules, receive summer meals from food trucks

- Families wait days to receive free dental care at tent clinics where buckets of pulled teeth pile up

- Hospitals charge the poor and uninsured full price for the same medical care the rich and insured receive at a steep discount

- A cancer-stricken Senator who's been on the receiving but never the giving end of compassion, votes to put in motion a vote that will make health care more expensive for the poor, sick and elderly

Avik Roy, Paul Ryan, Mike Pence, Tom Price and other conservatives talk about the freedom people will have to buy only the health insurance they can afford even if it's crappy coverage. That's the equivalent of saying that it is okay for families to pay rent at market rates for a house without a working toilet, broken windows and holes in the walls. These guys use the traditional definition of American Identity, freedom, to justify withholding legitimate government services and investment in its citizens.

Conclusion

Why doesn't America cringe at the thought of buckets full of rotten teeth and decide that's not what America is? Why doesn't America say that even though there is a market for a specific service, we won't let the lucky take advantage of the unlucky? Why isn't America ashamed that it believes more in the principle of freedom to die prematurely than providing basic health care to everyone?

America talks a good talk about democracy and freedom, but the world sees all the bad stuff too. They see the wretched conditions of America's poor communities. They see poverty, gun violence and a country unwilling to solve its health care access and cost problems. They see America for what it does, not what it says. Continue Reading...

The Health Care Reform Fight Is Just Beginning For Some Of Us

While the health care reform debate stalls in the Republican-majority Senate, individuals health insurance purchasers like me are left wondering what's next. Will Health and Human Services Secretary (HHS), Tom Price, miraculously develop a base level of professionalism and sense of duty to administer the Affordable Care Act (aka, Obamacare), the law of the land, for now, the way it was intended? Will Republicans restore the funds for the risk corridors so that insurers are certain that the government will cover losses they may incur? Will HHS role out a robust national open enrollment program for the exchanges and will they staff the effort appropriately? Or will the Senate, like the House, find a way to pass their awful health care bill, the

We, I, need answers to these questions soon because the fall health plan open enrollment season is just a few months away. My current health insurer has already sent me a good luck because we won't be here for you next year letter. And health insurance companies need answers to these questions now to make decisions about what, if any, plans they will offer to individual health plan purchasers.

Reason To Be Afraid For The Future Of Individual Health Plans

It's so disheartening to witness long-term Republican lawmakers and the White House react so vindictively to their current legislative debacle. After seven years of ranting about the awfulness of Obamacare and promising a better replacement, they delivered bupkis. But don't expect these guys to hang their heads in shame, that's a completely unfamiliar emotion to them. In fact, they can't even call their failure a failure. This is a line from the official statement put out by the Majority Leader's office on the Obamacare repeal vote.

" Regretfully, it is now apparent that the effort to repeal and replace the failure of Obamacare will not be successful."

In other words, Obamacare, which provided health insurance and health care to millions of people, is a failure but the seven-year long Republican effort that created the unpassable Trumpcare is not. The fact that McConnell refuses to acknowledge that Republicans do not have a better alternative to Obamacare that they are all willing to vote for makes me queasy.

And what's even scarier about the future of the individual health insurance market is that where McConnell leaves off in his hypocrisy and projection, Trump picks up with his mean, hateful, nastiness. Since being elected, (gag) Trump has boasted about letting 'Obamacare explode,’ ‘die on its own,’ or ‘fail,’ as he and his fellow Republican liars and obstructionists do everything they can to undermine the law. He threatened explosion when the House wavered in passing their crappy health care reform bill, the American Health Care Act (AHCA); and now he's threatening the same thing now that the Senate's bill is down and out (for now). I think Trump is dumb enough to try this strategy, and with his devil's helper, HHS Secretary Tom Price, things could spiral out of control quickly for people like me. Continue Reading...

If Only Conservatives Would Demonize Health Care Prices Instead Of The Poor

Republican Congressman Mo Brooks of Alabama wants us to "

This healthy people lead good lives, sick people lead bad lives is just updated phraseology for the same old moralizing nonsense conservatives use to demonize the poor and revere the rich. This type of thinking is so stupid and inapplicable in the real world. There are millions of healthy people who lead good lives that get sick. My best friend in the world was one of those people. She was active, did yoga regularly, ate organic, had an active social life and had a sharp mind. But one day she was diagnosed with cancer, and I lost her. This is a story repeated many times every day yet we still have jerks like Brooks that would rather use hateful language against the poor than address the unnecessarily high prices charged by hospitals and medical care providers.

You see politicians and doctors want us to believe the problem of unaffordable health care is our fault. If we only lead good, healthy lives, no one would need expensive, government-paid health care, says the politician. If we engaged in healthy behaviors and avoided unhealthy behaviors, we wouldn't suffer from expensive chronic diseases, says the doctor. And these politicians and doctors may have valid points—health care would be less expensive if we all lead healthy lives. But what world do these politicians and doctors live in? Who are these perfect, healthy people who do everything right in life? So instead of promoting this myth of the good, healthy, righteous, never need health care super-human being that does not exist, I wish Congressman Brooks and others like him would join us in the real world. A world where real good people, rich and poor alike get sick, sometimes really sick, and need expensive medical care.

The Alabama Congressman could address the financial limitations of high-cost medical innovations. About how much is too much medical innovation for the nation's pocketbook to cover? He could bring up for conversation why we require American doctors to obtain a Bachelor's degree before starting their medical degree education when many other industrialized nations do not. The cost of a medical education in America is the main justification doctors use for their high salaries. Mr. Brooks could learn more about the impact of socioeconomic factors on a person's health and support public policies to address these issues. He could also say that Americans should not pay hundreds of thousands of dollars for heart attack treatment. But he doesn't focus on any of these issues. Continue Reading...

Now Is The Time To Start Talking About Health Care Rationing

We are right to mock the hypocrisy of elected Republican officials that criticize the Affordable Care Act (aka Obamacare) for leaving millions of individuals uninsured and doing little to address the high cost of health insurance. Instead of creating policies to address these two Obamacare shortcomings, Republicans decided to exacerbate them by withholding funding to insurance companies that all but ensure that premiums will rise even higher and fewer individuals will have health insurance. We are also right to sneer when conservative intellectuals and Libertarians extol the virtues of a so-called free-market health care system where people are free to buy or not to buy any level of health insurance, and from any location they want. When the reality is that health insurers aren't in the habit of offering a la carte health plans. There's also the issue of opaque pricing with “free market health care.” Another issue with conservative and Libertarian views on health care is that half of the purchasers can buy insurance at a significant discount because of the workplace health insurance premium tax exclusion and the other half have no such benefit.

But at some point, and I think the time is now, Obamacare supporters and proponents of single payer or universal health care will have to realistically and publicly address how their proposed policies will deal with the problems of health care costs and affordability. Unlimited health care at any cost paid for by the government is not a realistic option, and no such system exists anywhere in the world. There are and should be limits on the amount of medical care an individual receives if they are not paying for it or if doctors and hospitals determine additional care would have no meaningful impact.

Our current U.S. health care system already places limits on the amount and form of medical care individuals receive. Sometimes these decisions are based on ability to pay the cost of care, and at other times they are based on medical science. However, this approach of rationing medical care won't be sufficient in a Medicare For All style system. Rationing of medical care will have to be front, and center of any government paid health care system. But that is not to say that people will not have access to care the government won't pay for; they are free to purchase health insurance or health care individually.

Some people may believe that a government codified system of medical care rationing harms the poor and favors the rich. Not necessarily. First, the poor won't likely pay anything for their medical care, and they will have access to preventative and continuous care that should improve their health status. Second, the poor won't have to pay for costly medical innovations, one of the real drivers of outrageous U.S. health care costs, but they will benefit from them. And third, the stigma applied to government-provided health care is diminished and so is the incentive for doctors and hospitals to treat the poor differently.

Right now proponents of government-paid health care for all our engaged in a battle to keep the poor from losing access to medical care. They may feel that they have to accomplish this goal first before they can start the conversation about their ideal health care system. Meanwhile, opposers of government-based health care use the socialists, communists, and hippie-dippy, out-of-control spending argument to make universal coverage look less attractive than the status quo. And I fear they are winning this argument because of a weak counter-argument of a greedy, evil opposition. Continue Reading...

The Republican You Either Don't Need Or Want Health Insurance Reform Bill

We will never know what the private health insurance market would look like today regarding cost and affordability if the Affordable Care Act (aka Obamacare) never became law. However, there is every reason to believe that

Very soon, Republican elected officials will likely pass a health care bill, or tax bill if you prefer, that will return us to the health insurance status quo, but with a twist. The Affordable Health Care Act (AHCA) passed by the House and the Better Care Reconciliation Act (BCRA) proposed by the Senate make the pre-Obamacare health care status quo look not so bad. The BCRA effectively makes individual health insurance plans worthless.

The Better Care Reconciliation Act allows health insurance companies to get away with paying barely half the cost of medical care while charging individual purchasers more than they currently pay in premiums, copays, deductibles, and coinsurance. These provisions in the bill are not just a case of more money for less coverage; they are an attempt to eliminate the individual market for all but the wealthy. Furthermore, these features of the bill are a way for the government to pay less in premium subsidies because people who can't afford these skimpy plans will drop out of the individual market altogether.

This Law (BCRA) Stinks

When Bill Clinton called Obamacare, "the craziest thing in the world," he was referring to the fact that the law offered no financial help to purchase health insurance for millions of individuals. These are people like me that didn't qualify for Obamacare subsidies, Medicaid, Medicare or the employer health insurance tax exclusion. We have to pay 100% of the cost of our health insurance even though most of us are not wealthy. Meanwhile, Obamacare supporters, especially the ones responsible for administering the ACA, downplayed the size of this group or claimed that they would get around to helping us eventually.

After winning the majority of seats in the House and Senate and electing a Republican president, Republican officials seized on Bill Clinton's statement claiming their health care reform bill would eliminate the craziness. Continue Reading...

The Splintered Health Care Policy Goals of Conservatives Are All Bad For The Poor

Before the passage of the Affordable Care Act (aka Obamacare), America had not had a conversation about health care policy in decades. So it's understandable that many elected officials lacked knowledge about America's health care system and assumed it was performing as intended. From what they understood the health care status quo met the needs of the wealthy, professional and middle classes. And the poor, elderly and veterans had government-provided insurance.

But looks can be deceiving; individuals without any group-provided insurance were left to the mercy of the health insurance market. A market that left over 40 million of them uninsured. Obamacare came along and upset the peace of health care policy reform at the best and worst possible time.

It was the best time for an Obamacare-type law because about 40 million Americans did not have health insurance and Obamacare provided coverage to almost 40% of them. And it was the worst time for an Obamacare-type law because the country was and is so divided on most major public policy issues. Major health care reform was introduced in a politically polarized era that became even more polarized when Trump won the presidential election, and the Republicans won a majority of Senate and House seats.

More Than A House Divided

The Republican/conservative health care policy stance is much more splintered than it is among Democrats/liberals. Democrats want Medicare or Medicaid for All, universal health care or single payer. Or maybe they just want more federal funding for the Obamacare exchanges. It depends on which group of Democrats you ask, but at least they all want a health care reform policy that expands coverage to all Americans, Republicans disagree with Democrats on the very definition of universal access to health care. Remember when the Republican Party stupidly referred to health insurance/care access as "freedom?"

But idiotic catchwords aside, Republicans and conservatives also disagree with each other on the policy goals of health care reform. First, there is Senate Majority Leader, Mitch McConnell's (a real life villain) view that replacing Obamacare is the ultimate policy goal. He couldn't care less about the contents of any health bill and its impact on the public. His only health care reform policy objective is to convince enough Republican senators to pass an Obamacare repeal bill quickly. Continue Reading...

Americans Never Really Wanted A Fairer Health Care System, And They're Not Going To Get One Anytime Soon

A recent New York Times article laments the "halfhearted opposition" to the pending passage of the American Health Care Act (AHCA, aka Trumpcare) by powerful groups such as doctors, nurses, hospitals and patient advocates. Health policy experts condemn the "fast-tracking" of the ACHA in the Senate. And the Jeff Sessions' hearings and other Russia collusion noise, crowd out national reporting on the AHCA as the Senate is weeks away from passing their health care reform bill.

The AHCA passed by Congress and currently undergoing revisions in the Senate, rewards the healthy and wealthy and punishes the sick and poor. Some people are appalled and baffled by the impending passage of legislation that brings more inequality into an already unequal system. Isn't it more sensible to provide the most financial assistance to people that need the most health care? Well this is America, where a near majority believes it's okay that the rich can afford better health care than the poor.

The Poor Cost Too Much

Many people think the sick are responsible for their illness(es) due to their engagement in "voluntary health risks" or "changeable behaviors." Never heard these terms before? Me neither. I guess using the term unhealthy lifestyle didn't sufficiently make the point that sickness is a choice, and an expensive one at that.

By some estimates an unhealthy lifestyle cost hundreds of billions of dollars each year in medical care. A recent study contracted by General Electric estimated the cost of cancer care due to an unhealthy lifestyle at around $34 billion per year. Other studies put the annual costs of treating alcohol abuse at an estimated $176 billion, smoking at $137 billion and obesity at $147 billion (2008 number for obesity). These issues—cancer, alcohol abuse, smoking and obesity—costs nearly a half trillion dollars in health care each year.

But cost concerns are not what allow the Republican Congress and Senate to easily take away health insurance from the sick and poor. The truth is that despite the passionate town halls, we don't want the poor to live as long as the wealthy. We would save money if they did not. According to the Congressional Budget Office (CBO) score of the AHCA, that savings is about $3 billion, to start (represents reduction in Social Security payments due to early deaths). Continue Reading...

Health Care Reform Sausage-Making Grinds On

Overpricing and